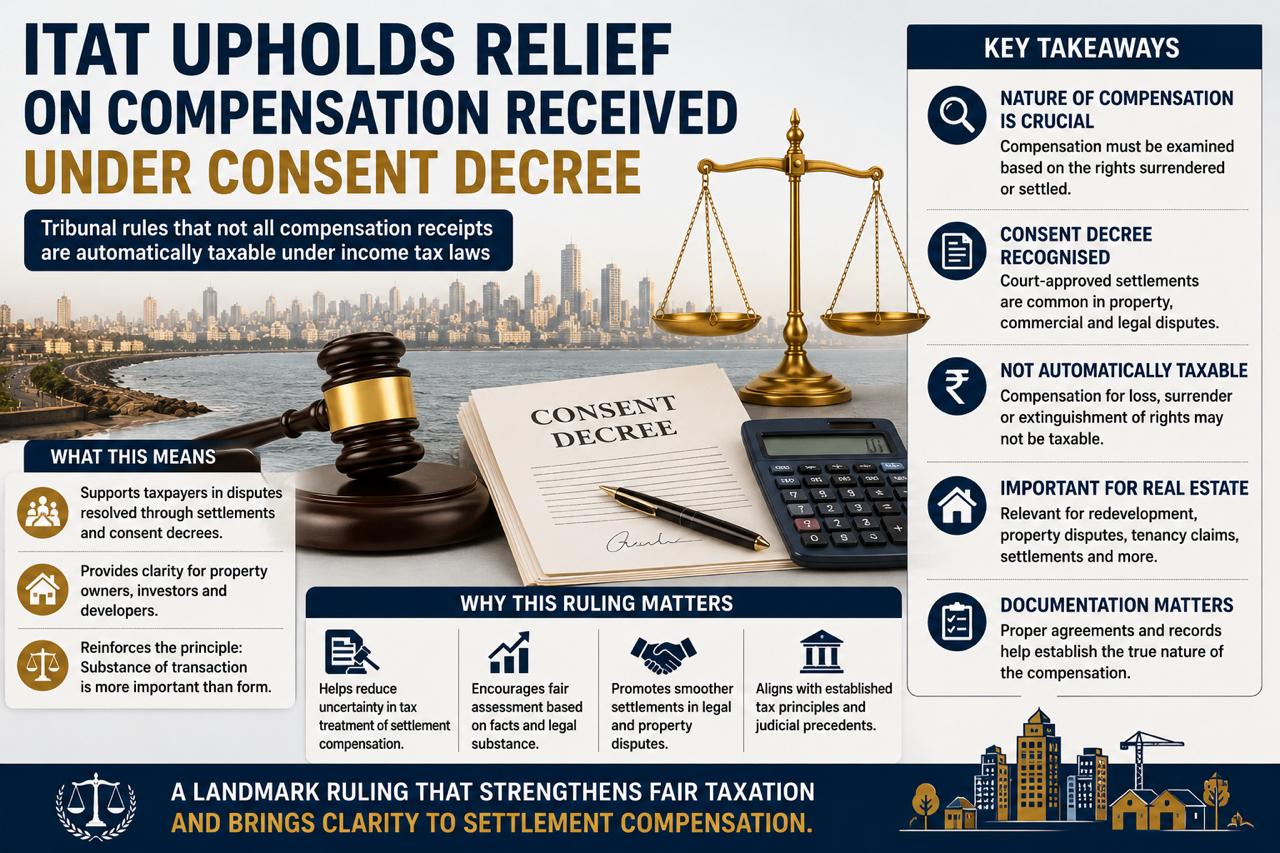

ITAT Upholds Tax Relief on Compensation Received Under Consent Decree

ITAT Upholds Relief on Compensation Received Under Consent Decree

In a significant ruling with implications for property owners, investors, and taxpayers, the Income Tax Appellate Tribunal (ITAT) has upheld tax relief on compensation received pursuant to a consent decree. The decision highlights the importance of examining the true nature of a compensation payment before determining its tax treatment.

The ruling reinforces a long-established principle of tax law that compensation received for the loss, surrender, or extinguishment of certain rights may not always constitute taxable income. Instead, courts and tribunals must examine the purpose and character of the payment rather than relying solely on the fact that money has been received.

The judgment is particularly relevant for disputes involving property rights, redevelopment agreements, commercial settlements, and compensation arising from litigation.

What Is a Consent Decree?

A consent decree is a court-approved settlement agreement between parties to a dispute. Rather than proceeding through a lengthy trial, the parties agree to resolve their differences through mutually accepted terms, which are then recorded and approved by the court.

Such settlements are common in property disputes, redevelopment matters, inheritance claims, partnership disagreements, contractual disputes, and commercial litigation.

Because compensation payments under consent decrees can arise from a wide variety of circumstances, their tax treatment often becomes a matter of legal interpretation.

Nature of Compensation Becomes Crucial

The key issue before the tribunal was whether the compensation received should be treated as taxable income or whether it represented compensation for the relinquishment or settlement of rights.

Tax authorities frequently examine compensation receipts to determine whether they arise from a revenue transaction, which may be taxable, or from the settlement of a capital asset or legal right, which could attract a different tax treatment.

The ITAT's decision underscores that the substance of the transaction is more important than its form. The mere receipt of compensation does not automatically create a tax liability.

Why the Ruling Matters for Property Owners

Property disputes often result in negotiated settlements involving compensation payments. Redevelopment projects, land ownership disputes, tenancy claims, inheritance matters, and title conflicts frequently conclude through consent decrees rather than full court proceedings.

In such cases, the tax implications of compensation can be substantial. The tribunal's ruling provides guidance that compensation must be evaluated based on the rights being surrendered, transferred, or extinguished.

For property owners, understanding the distinction between capital receipts and taxable income can significantly affect the financial outcome of a settlement.

Implications for Redevelopment Projects

Mumbai's redevelopment-driven real estate market regularly witnesses disputes involving societies, landowners, tenants, developers, and investors. Many of these disputes are resolved through negotiated settlements approved by courts or other authorities.

Compensation paid under such arrangements may relate to rehabilitation rights, development rights, tenancy claims, relocation agreements, or settlement of legal disputes.

The ITAT's decision highlights the importance of properly structuring and documenting such transactions to ensure that the nature of compensation is clearly established.

Documentation Remains Critical

One of the most important lessons emerging from tax disputes involving compensation is the need for comprehensive documentation. Courts and tribunals typically examine settlement agreements, court orders, consent terms, property records, and supporting evidence to determine the character of a payment.

Well-drafted agreements that clearly explain the purpose of compensation can help reduce uncertainty and minimise future disputes with tax authorities.

Taxpayers involved in significant settlements should therefore ensure that the legal and commercial intent behind the payment is properly documented.

A Reminder That Tax Treatment Depends on Facts

The ruling does not mean that all compensation payments are exempt from tax. Rather, it reinforces the principle that each case must be assessed based on its specific facts and circumstances.

The taxability of compensation depends on factors such as the nature of the rights involved, the purpose of the payment, the underlying transaction, and the applicable provisions of tax law.

As a result, taxpayers should avoid assuming that compensation receipts will automatically qualify for relief and should seek professional advice where necessary.

What It Means for the Real Estate Sector

The judgment is particularly relevant in a city like Mumbai, where property-related disputes and redevelopment settlements frequently involve substantial compensation amounts. Greater clarity regarding tax treatment can help parties negotiate settlements more effectively and assess their financial implications with greater certainty.

For developers, landowners, societies, and investors, the ruling serves as a reminder that legal structuring and tax planning are increasingly important aspects of complex property transactions.

As redevelopment activity continues to expand across the Mumbai Metropolitan Region, tax treatment of settlement compensation is likely to remain an important issue.

Expert View

"Compensation received under a settlement or consent decree cannot be viewed in isolation. The real question is what right is being surrendered or settled. The ITAT's ruling reinforces the principle that tax authorities must examine the substance of a transaction before determining its taxability. For property owners and developers, careful documentation remains essential." — Sandeep Sadh

Looking to buy or rent in Mumbai?

Talk to Mumbai's oldest property portal — RERA-verified listings, real availability, instant answers.

More Property News

💬 Comments