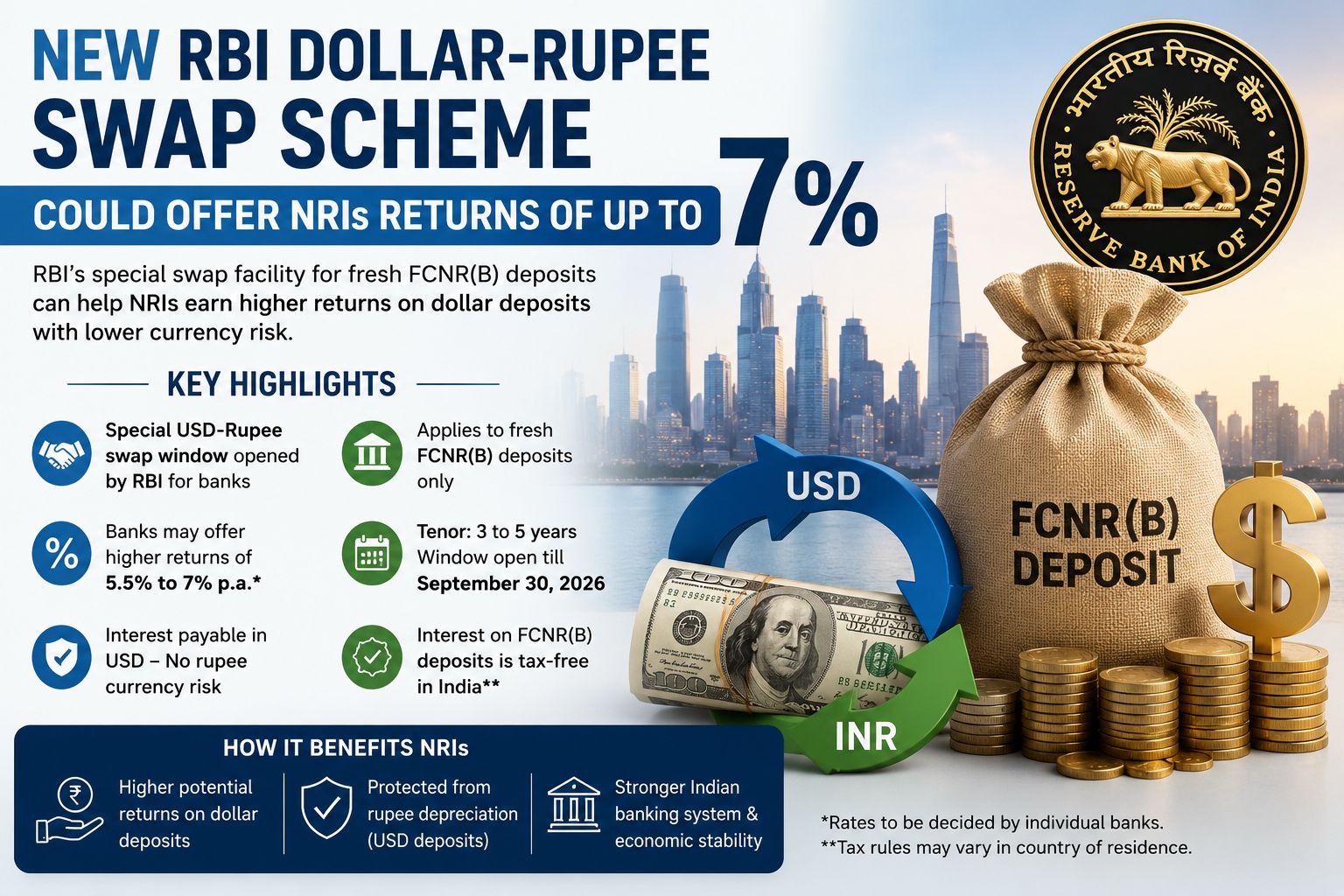

RBI Dollar-Rupee Swap Scheme Could Offer NRIs Higher Returns on Dollar Deposits

RBI Opens Special Dollar-Rupee Swap Window for NRI Deposits

The Reserve Bank of India has introduced a special US Dollar-Rupee swap facility aimed at attracting fresh foreign currency deposits from Non-Resident Indians. The move is designed to encourage more stable dollar inflows into India at a time when currency volatility, global uncertainty, and pressure on the rupee remain important policy concerns.

The scheme is focused on fresh FCNR(B) deposits, which are foreign currency deposits maintained by NRIs with Indian banks. Under this facility, banks can raise dollar deposits from NRIs and swap those dollars with the RBI, reducing the currency risk and hedging cost that normally limits the returns banks can offer depositors.

The facility is expected to allow banks to offer significantly more attractive returns on dollar deposits, with possible yields estimated around 5.5% to 7% per annum, depending on the bank and deposit terms.

What Is an FCNR(B) Deposit?

FCNR(B) stands for Foreign Currency Non-Resident Bank deposit. It is a fixed deposit held by NRIs in foreign currency, such as US dollars, with an Indian bank.

Unlike NRE or NRO deposits that are usually rupee-denominated, FCNR(B) deposits allow NRIs to keep their money in foreign currency. This means the depositor does not face rupee depreciation risk because both the principal and interest are repaid in the same foreign currency.

For NRIs with dollar savings, this structure can be attractive because it combines Indian banking access with foreign currency protection.

How the New Swap Scheme Works

Normally, when banks accept foreign currency deposits and use those funds within India, they must manage currency risk. This hedging cost can be high and often reduces the interest rate banks are able to offer NRIs.

Under the RBI's special swap facility, banks can swap their fresh dollar inflows with the central bank at a fixed arrangement. This reduces or removes a major part of the hedging burden for banks.

Because the RBI absorbs the currency mismatch through the swap structure, banks may be able to pass on part of the benefit to NRI depositors in the form of higher interest rates.

This is why the scheme could nearly double the returns available on certain dollar deposits compared with regular FCNR(B) rates.

Potential Returns for NRIs

Current FCNR(B) deposit rates are generally lower because banks factor in hedging costs and global interest-rate conditions. With the new swap facility, returns could move into the 5.5% to 7% range for eligible deposits.

However, the exact interest rate will not be fixed by the RBI. Individual banks will decide their own rates based on their funding requirements, competition, deposit tenor, and internal pricing strategy.

NRIs should therefore compare actual offers from different banks before investing.

Deposit Window and Tenor

The facility is expected to remain open for a limited period, making it a time-bound opportunity for eligible NRIs. Reports indicate that the window is available until September 30, 2026.

The scheme is expected to apply to fresh FCNR(B) deposits with tenors of three to five years.

This means NRIs looking to participate may need to make decisions within the specified window and be comfortable locking funds for a medium-term period.

Why RBI Has Introduced the Scheme

The scheme is aimed at attracting stable dollar inflows into India. When NRIs place foreign currency deposits with Indian banks, it strengthens the country's foreign currency resources and supports financial stability.

The move comes at a time when global market volatility, oil price concerns, and currency pressure have made foreign exchange management more important.

A similar strategy was used in 2013, when India attracted significant NRI dollar deposits during a period of rupee pressure. That earlier window helped improve foreign exchange reserves and stabilise sentiment.

The current scheme appears to follow a similar logic by encouraging NRIs to bring more dollar funds into the Indian banking system.

Why This Matters for the Rupee and Banking System

Fresh dollar inflows can support India's external position and help reduce pressure on the rupee. They also provide banks with additional foreign currency resources.

For the banking system, lower hedging costs make it easier to raise dollar deposits competitively. For NRIs, this can translate into better returns without taking direct rupee currency risk.

The scheme therefore benefits multiple stakeholders: NRIs receive higher potential returns, banks gain access to foreign currency funding, and the country receives more stable dollar inflows.

Tax Treatment for NRIs

Interest earned on FCNR(B) deposits is generally exempt from tax in India for eligible NRI depositors. This tax treatment can make the product more attractive compared with taxable investment options.

However, NRIs should also check tax rules in their country of residence. A deposit that is tax-free in India may still be taxable overseas depending on local tax laws.

Professional tax advice is important before making large deposits.

Important Risks and Conditions

While the returns may look attractive, NRIs should understand the fine print before investing.

The rate is not guaranteed by the RBI. Banks will decide the final rate.

The deposit may require a medium-term commitment of three to five years.

Premature withdrawal may be restricted or may reduce returns, depending on bank rules.

Deposit insurance protection in India is limited, which may not fully cover large foreign currency deposits.

NRIs should also evaluate the strength of the bank, liquidity needs, and tax treatment in their country of residence before committing funds.

Impact on Real Estate and NRI Investment Sentiment

Higher returns on dollar deposits could improve financial confidence among NRIs and increase their engagement with Indian financial markets. A stronger NRI deposit flow can also support broader capital inflows into India.

For the real estate sector, the impact may be indirect but important. NRIs are a key buyer segment in markets such as Mumbai, Thane, Navi Mumbai, Pune, Bengaluru, Hyderabad, and Delhi-NCR.

When NRIs feel more confident about India's financial stability and currency management, they may also become more comfortable evaluating long-term investments such as residential property.

Stable currency conditions and attractive banking products can support NRI participation in India's housing market over time.

What NRIs Should Do Now

NRIs interested in the scheme should monitor announcements from major Indian banks offering FCNR(B) deposits. They should compare interest rates, deposit tenors, withdrawal rules, tax treatment, and bank credibility before making a decision.

The scheme may be particularly useful for NRIs holding idle dollar balances who want better returns without converting funds into rupees.

However, it should be treated as a fixed-income opportunity rather than a guaranteed high-return investment.

Expert View

"The RBI's dollar-rupee swap facility is designed to attract stable foreign currency deposits while reducing hedging costs for banks. For NRIs, it could create an opportunity to earn higher returns on dollar deposits without taking rupee currency risk. The scheme may also improve confidence in India's financial system and indirectly support long-term NRI participation in Indian real estate and investment markets." — Sandeep Sadh

Looking to buy or rent in Mumbai?

Talk to Mumbai's oldest property portal — RERA-verified listings, real availability, instant answers.

More Property News

💬 Comments